- English

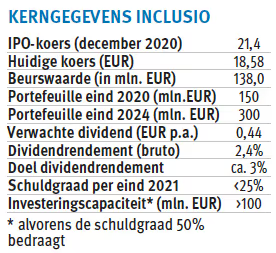

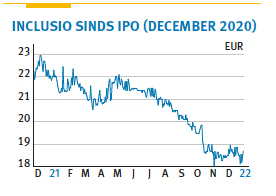

Inclusio, the residential GVV with a focus on affordable (social) rental housing, made its IPO debut in December 2020 at an IPO price of EUR 21.4. For now, the GVV could not convince investors. The stock had the worst stock market performance of all GVVs in 2021 and is now trading even 15-20% below its intrinsic value. We had a conversation with the CEO, Marc Brisack.

A frustrating course performance after more than one year....

MB: We had decided at IPO to take the intrinsic value as the IPO price. This certainly did not seem excessive to us given some comparable IPOs quoted at a (nice) premium. The expected dividend yield of 2% (gross) was - admittedly - rather on the low side. But we are counting on a 3% gross yield as early as next year. That's not nothing.

Yes, but that is lower than comparable GVVs?

MB: This obviously depends on the segment in which we operate. Our goal is to provide affordable housing (nvdr: about 80% of revenue), as well as housing for the disabled and "social infrastructure" (including shelters). We do not pursue profit maximization. The lower return is also explained by our low risk profile. After all, we rent our properties to social landlords (SVK) on very long terms. These are sometimes contracts of up to 27 years with a lot of rental flexibility and an occupancy rate of 100%. We rent our properties at a nice discount to the prevailing market rent. The SICAVs are then responsible for their management (collection of rent, maintenance...).

On the positive side, after more than one year you are beyond the targets included in the prospectus.

MB: We had indeed anticipated having a portfolio of 230 mln. EUR (150 mln. EUR at the IPO). That will be at least 250 mln. EUR. And our balance sheet can easily handle that. At the end of 2021, the debt ratio was less than 25%. That gives us an additional investment capacity of over 100 mln. EUR before reaching the 50% limit. This is the upper limit set by the Board of Directors.

So a capital increase is not an issue in the coming years?

MB: We can certainly continue under our own steam until 2024. After that we cannot rule out raising fresh capital. By then, of course, we hope that the share price will again be close to intrinsic value.

How will the dividend evolve in the coming years?

MB: For now, we haven't defined a dividend policy, but we do want to pay out 3% gross starting next year. After all, we continue to grow nicely and achieve nice margins. After all, the portfolio we are building offers a gross rental yield of about 4.3% while we are borrowing at only 1.8%. That means a nice margin of 250 basis points.

OUR OPINION:

At the IPO in late 2020, we had recommended not subscribing because the first dividend would not be paid until spring 2022. Moreover, we feared share price pressure should reference shareholder Integrale (14.3% of capital), which has recently gone into liquidation, start dumping its stake. That stake was transferred at the end of 2021 to Monument Assurance Belgium, an insurer that may remain a long-term investor.

That Inclusio quotes at a discount against the most comparable player (Home Invest Belgium) makes sense. HIB achieves a gross rental yield of about 5%, has a larger portfolio, a higher dividend yield and benefits from regular arbitrages (sales of mature properties) to boost profits. But a 15% to 20% discount to intrinsic value is starting to become quietly attractive. Inclusio is growing at a solid pace and recently started its own developments, on which it is achieving higher margins. Inclusio targets a portfolio of about EUR 300 mn. EUR by 2024 and has a low debt ratio of less than 25%. So there is no fear of a capital operation.

Since profit maximization is not an end in itself for Inclusio, as an investor you have to settle for a slightly lower dividend yield, but which nevertheless remains solid. At the end of November (at prices below EUR 19), we raised our recommendation to "first position" (H+ 1). Management has also recently started buying its own shares. When placing an order for this highly illiquid stock, it is best to work with limit orders.

This article was reproduced with the permission of the publisher, all rights reserved. Any reproduction must be the subject of specific permission from the License2Publish management company: info@license2publish.be

Photo gallery

No items found.